The Exit Isn't a Door Anymore. It's a Hallway of Windows.

Why employees, founders, and early backers no longer wait for the IPO to get paid.

For years, the industry talked about liquidity as if it lived at the end of the story. First you invest, then the company grows, then one day there's an IPO or an acquisition, and only then does anyone get paid.

I never fully believed that. Startups aren't built in one clean arc. They're built over a decade or more, across many rounds, through changing teams, early employees, angels, seed funds, and founders whose entire net worth sits locked inside one illiquid company far longer than most people expect. If the building happens continuously, why should the liquidity arrive all at once, at the very end?

The market is finally catching up to that question. According to Carta, startups on its platform ran 396 tender offers in 2025, up 62% from the year before, with nearly one in five coming from companies at Series E or later. And the behavior inside those offers is shifting too: the median subscription rate, the share of buyer demand that sellers were willing to meet, climbed from 73.8% in early 2021 to 99.9% by the first half of 2025. Sellers used to hold back. Now, when a window opens, they walk through it.

That's not just a secondary-market statistic. It's a sign that private companies are starting to treat as deliberate design something they used to treat as an afterthought: letting people sell.

The Old Rhythm Is Under Pressure

The classic venture loop was simple: invest, grow, exit, distribute, repeat. That loop still exists, but the timing has stretched. Companies now stay private for ten, twelve, fifteen years. IPO windows open and close unpredictably. And the longer a company stays private, the more people it leaves holding paper they can't touch.

An employee who joined at Series A may be five years vested with nothing to show a bank. A founder can be worth a fortune on paper and stretched thin in real life. An angel who took the first risk, or a seed fund that needs to return capital to its own investors, may be waiting on an exit that keeps slipping another two years down the road.

The bargain startup equity has always asked for, take the risk, accept the illiquidity, wait for the big outcome, still works. But when the wait runs past a decade, the bargain quietly changes. People need a release valve long before the final door.

The IPO Used To Do Too Many Jobs

Part of why liquidity felt like an endpoint is that the IPO was overloaded. It was never one thing. In a single event, an IPO was a fundraising round, a branding moment, a governance transition, a price-discovery event, an employee payday, an investor exit, and the moment LPs finally saw cash come back.

One event, seven jobs. No wonder everyone waited for it.

But private markets have changed. Late-stage companies now raise enormous sums while staying private. Valuations get set in rounds and secondary marks, not only at listing. And employees and early backers increasingly need to sell years before anyone rings a bell. So the functions the IPO used to bundle together are quietly separating. The IPO isn't disappearing, but it no longer has to be the only place liquidity lives. That's what I mean by unbundling the exit.

The Tender Offer Is The First Piece To Break Off

Of all those bundled jobs, the one splitting away most cleanly is letting people sell. And the tool doing it is the tender offer.

A tender offer is a formal, company-sponsored transaction that lets shareholders sell a set amount of stock at a set price. The important word is company-sponsored. Private shares aren't public shares, they aren't meant to trade freely every day. The cap table matters. Who owns the stock matters. Transfer restrictions, information rights, and founder control all matter.

So the real question was never "can someone sell their shares?" It's "can selling happen in a way that protects the company, respects existing shareholders, rewards the people who showed up early, and keeps the cap table clean?" A well-run tender offer answers yes. It creates partial liquidity without turning the stock into a free-for-all, a controlled window, not an open market.

That control is exactly why sellers are growing more comfortable stepping in. And liquidity, done right, doesn't have to break long-term alignment. A founder who takes a little off the table can afford to stay patient. An employee who gets partial liquidity starts trusting equity as real compensation again. An early fund that returns some capital keeps the flexibility to keep backing the company. Handled well, a window can strengthen the very alignment people fear it erodes.

Tender Offers Are Not The New IPO

It's tempting to say tenders are becoming the new IPO. Catchy, but wrong. Tenders don't create a public listing, or continuous trading, or public access, or the reporting and governance load of going public. They replace exactly one of the IPO's old jobs, letting people sell, and leave the rest alone.

That's the right way to hold it: a tender offer isn't a smaller IPO, it's a private liquidity window. Structured, partial, controlled, company-approved, time-bound. For a lot of late-stage companies, that's closer to what they actually need than a premature listing or a chaotic gray market in their shares.

The New Skill Is Liquidity Design

Here's what this changes for those of us who invest. For a long time, the craft of venture was mostly about entry, winning allocation, underwriting the round, getting into the best companies. Exit was a distant, administrative afterthought.

In a world where companies stay private for fifteen years, that no longer holds. Liquidity becomes part of the job: part of how you support founders, retain employees, manage the cap table, and keep early backers whole. The questions worth asking now aren't only "what's the exit?" but "what's the liquidity plan along the way?" Should this company open a window every couple of years? Who gets to sell, just employees, or angels and early funds too? How much can founders take, and when? These aren't small mechanics. They shape trust, incentives, and how long a company can keep building privately without pressure building up inside its own cap table.

The Risks Are Real

None of this means more liquidity is always better. A badly designed window creates more problems than it solves. Sell too early and it signals doubt. Let founders take out too much and investors question their conviction. Open it to some shareholders but not others and you breed resentment. Let in the wrong buyers and the cap table gets harder to manage, not easier.

There's a cultural risk too. Startups work partly because people are aligned around a long game. If liquidity becomes too frequent or too easy, people start thinking like traders instead of builders. So the goal isn't liquidity at all costs, it's enough to relieve the pressure, not so much that it dissolves the mission. That balance is the whole art.

The Exit Is Becoming A System

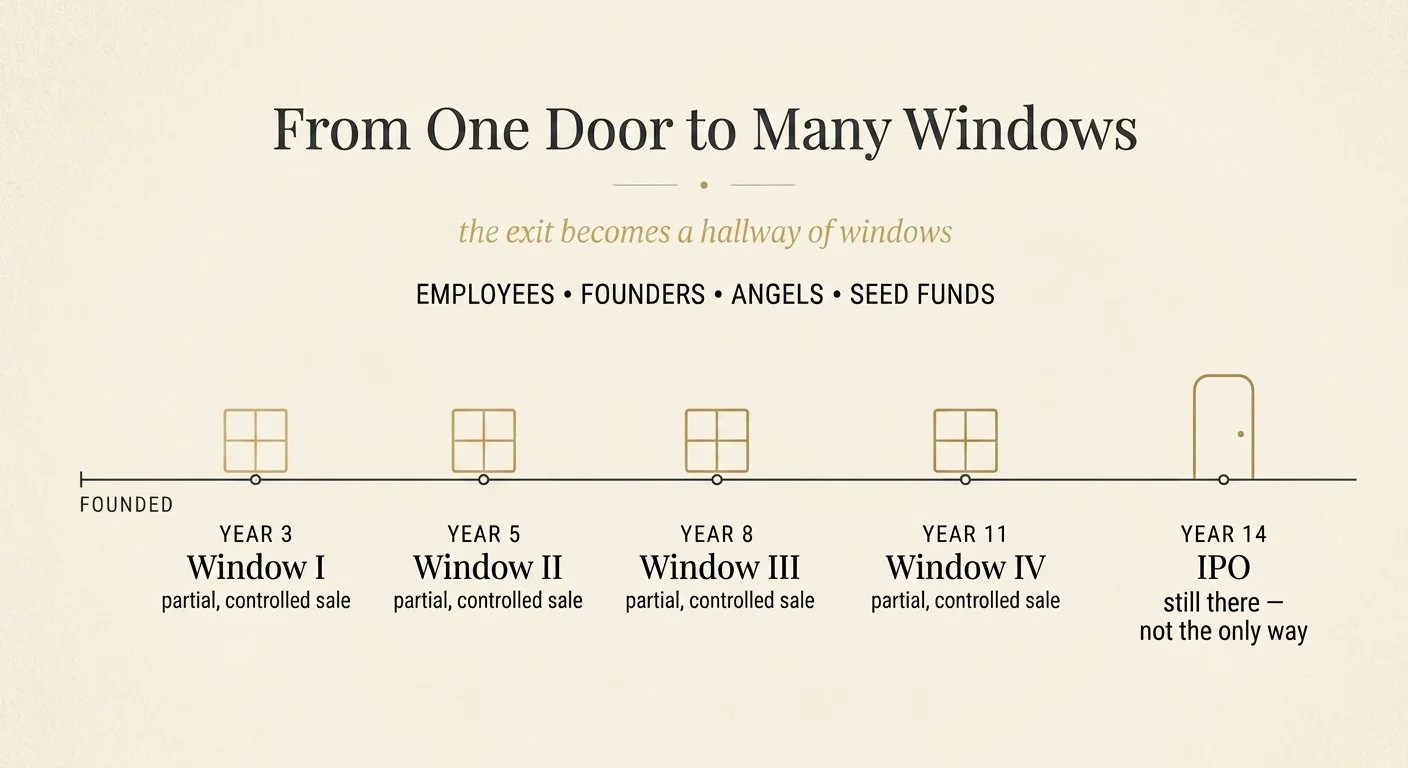

The old story imagined liquidity as a single door at the end of the hallway: build long enough, reach the door, and the story ends. The next era looks more like a hallway with windows along the way, one for the employee who showed up early, one for the angel who took the first risk, one for the seed fund that needs to recycle capital, one for the founder who needs enough security to keep going. And the final door is still there at the end, just no longer carrying all the weight.

That's the shift worth internalizing. Liquidity isn't the opposite of long-term building. Designed poorly, it distracts. Designed well, it makes the whole journey more durable. The best investors won't just help founders raise the next round, they'll help design the liquidity architecture for the company they're actually trying to build.

Because in the next era of venture, the exit isn't a single event at the end. It's a system. And the people who see that early will have the edge.