Retail Finally Got SpaceX. The Asymmetric Returns Were Already Gone.

Why the real money on SpaceX was made years before retail ever got a seat.

On June 12, 2026, SpaceX became a public company. It priced at $135 a share, closed its first day up 19% at $160.95, and ended the session worth more than $2 trillion, the sixth-most-valuable public company in the United States and the largest IPO ever recorded, raising roughly $75 billion (NPR, CNBC).

The headline everyone reached for was democratization. And on the surface, they were right to. SpaceX earmarked about 30% of its float for retail investors, roughly three times the usual mega-cap norm, routed through the brokerages ordinary people actually use: Fidelity, E-Trade, Schwab, SoFi (BitMEX, NBC News). For a company that spent nearly a quarter-century private, that is a genuine shift in IPO mechanics. Retail finally got a seat.

Here is the uncomfortable question a private-markets investor should ask anyway: a seat at what?

Access Arrived Exactly When The Asymmetry Left

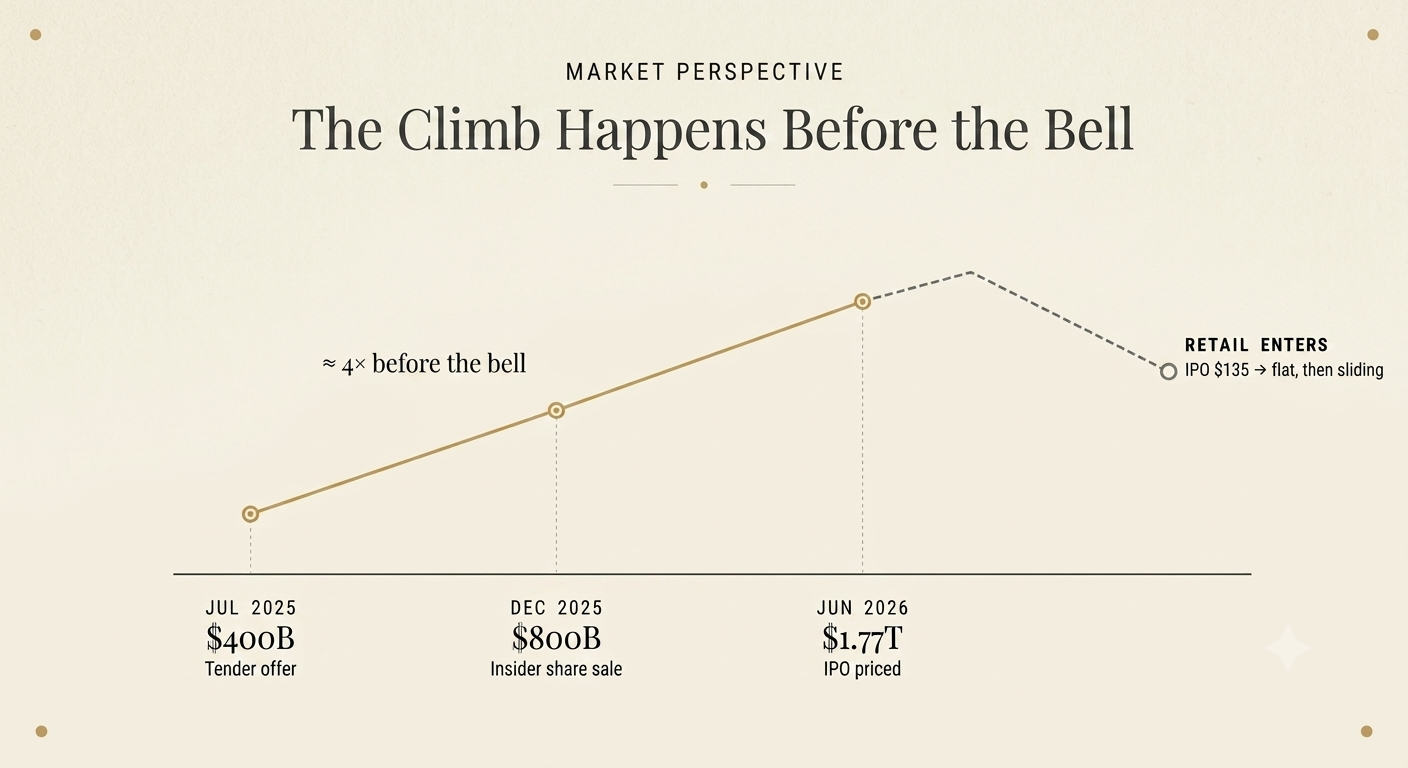

Value in a company like SpaceX is not created at the opening bell. It is created in the years before it, quietly, through late-stage rounds and twice-a-year tender offers that only a narrow circle of insiders and institutions can touch. Watch where the price actually moved:

July 2025 — a tender offer valued SpaceX at roughly $400 billion (Fortune).

December 2025 — an insider share sale roughly doubled that to ~$800 billion in under six months (Sacra, Bloomberg via phys.org).

June 2026 — the IPO landed at a ~$1.77 trillion valuation, above $2 trillion by the close of day one (Wikipedia).

Do the arithmetic on that ladder. An investor who accessed the July 2025 tender at ~$400 billion was sitting on more than a 4x mark by the time the stock rang the Nasdaq bell, in about eleven months. The December 2025 buyer at ~$800 billion roughly doubled in six. The retail investor who received an IPO allocation at $135 got a respectable first-day pop and then watched the stock run above $225 before sliding back toward the low $150s in the weeks that followed (Barchart). Modest gain for the allocated; underwater for anyone who chased it in the aftermarket.

Same company. Same rocket. Radically different returns, determined almost entirely by when you were allowed in.

And there is a reason those shares were available to buy at $400 billion in the first place: someone on the inside wanted out. Every private liquidity window is a transfer. An early employee, a founder, a seed fund reaching the end of its life, each trades a shot at the remaining upside for the certainty of cash today, and whoever sits on the other side of that window inherits the asymmetry they let go. The seller gets liquidity. The buyer gets the returns. Being early is rarely luck. It is being positioned to take the other side of that trade, and being allowed to.

This is the pattern that repeats across every marquee private name. By the time an S-1 is public, the business has already been priced, partially liquidated, and circulated among a small group of sophisticated buyers, sometimes at valuations an order of magnitude below where it lists. What looks like price discovery at the IPO is frequently price confirmation, the public meeting a number that the private market settled long ago (Invezz via TradingView).

The Gate Is Real, and The Issuers Control It

If you doubt how tightly upstream access is guarded, look at what Anthropic did in May 2026, weeks before its own confidential IPO filing. It formally warned eight secondary-market platforms, including Forge, Hiive and Sydecar, that they were unauthorised to trade its shares and that related transactions would be deemed invalid (IG).

Sit with that. In the single hottest asset class in the world, a company can simply declare which channels are allowed to transact its stock. Access to the best private opportunities is not a matter of having capital or even being accredited. It is a matter of being on the right side of a curated, relationship-gated door. The platforms selling "access" are not always the ones that have it.

The Exit Window Is Opening, and It Changes Nothing About The Upstream Game

The pipeline behind SpaceX makes this timely rather than academic. Anthropic filed confidentially on June 1, 2026, at a roughly $965 billion private valuation and is tracking toward a late-2026 listing; OpenAI followed about a week later, though after SpaceX's choppy debut it is reportedly weighing a slip into 2027 (Barchart, Yahoo Finance). A wave of trillion-dollar exits is forming.

But an exit wave does not democratize the entry. It simply marks the moment the asymmetry has already been harvested. Retail gets the confirmation; the curve was climbed years earlier by whoever held the shares through the private compounding. The lesson of SpaceX is not "private markets are opening up." It is the opposite: the returns that matter are captured before the door most people are waiting at ever opens.

Why This Is The Whole Point of Diwan

None of this is an argument against public-market participation. It is an argument for being early, and for being inside, which is precisely the problem Diwan exists to solve.

The mechanics that made SpaceX's early holders rich, tender access, secondary allocations, co-investment alongside the institutions that get the call first, are structurally out of reach for most qualified investors in our region, not because they lack capital, but because they lack the door. Curated access to those positions is the asymmetry. Everything downstream of it is just confirmation.

That is the entire thesis in one line: curated access, asymmetric returns. The SpaceX bell didn't disprove it. It rang it.