Deep Dive: Mapping the AI SDR Stack — Why the MENA Winner May Not Look Like the US Winner

I’ve been mapping the AI SDR category for a while now. Partly because it is an interesting space on its own, but also because this is usually how I explore any new domain as a VC. Before I form a view on where the money is, I try to map the full workflow. Who owns the data? Who owns the channel? Who owns the customer relationship? Who gets commoditized? Who captures the margin? And most importantly: where does the US playbook break when you move it into our region?

The AI SDR market looks noisy from the outside. Everyone is promising some version of the same thing: better prospecting, better personalization, more meetings, fewer humans. But once I started mapping it, I realized the first mistake was trying to place every company neatly into one box.

That is not how this market is evolving. Apollo is not just a contact database. It also does sequencing, follow-ups, calling workflows, LinkedIn touches, and CRM syncing. Clay is not just enrichment. It helps users find data, combine sources, run AI research, personalize outreach, and trigger downstream workflows. HeyReach is not only a LinkedIn sender. It can start from LinkedIn search and lead sourcing, then help enrich, sequence, and execute outbound across multiple sender accounts.

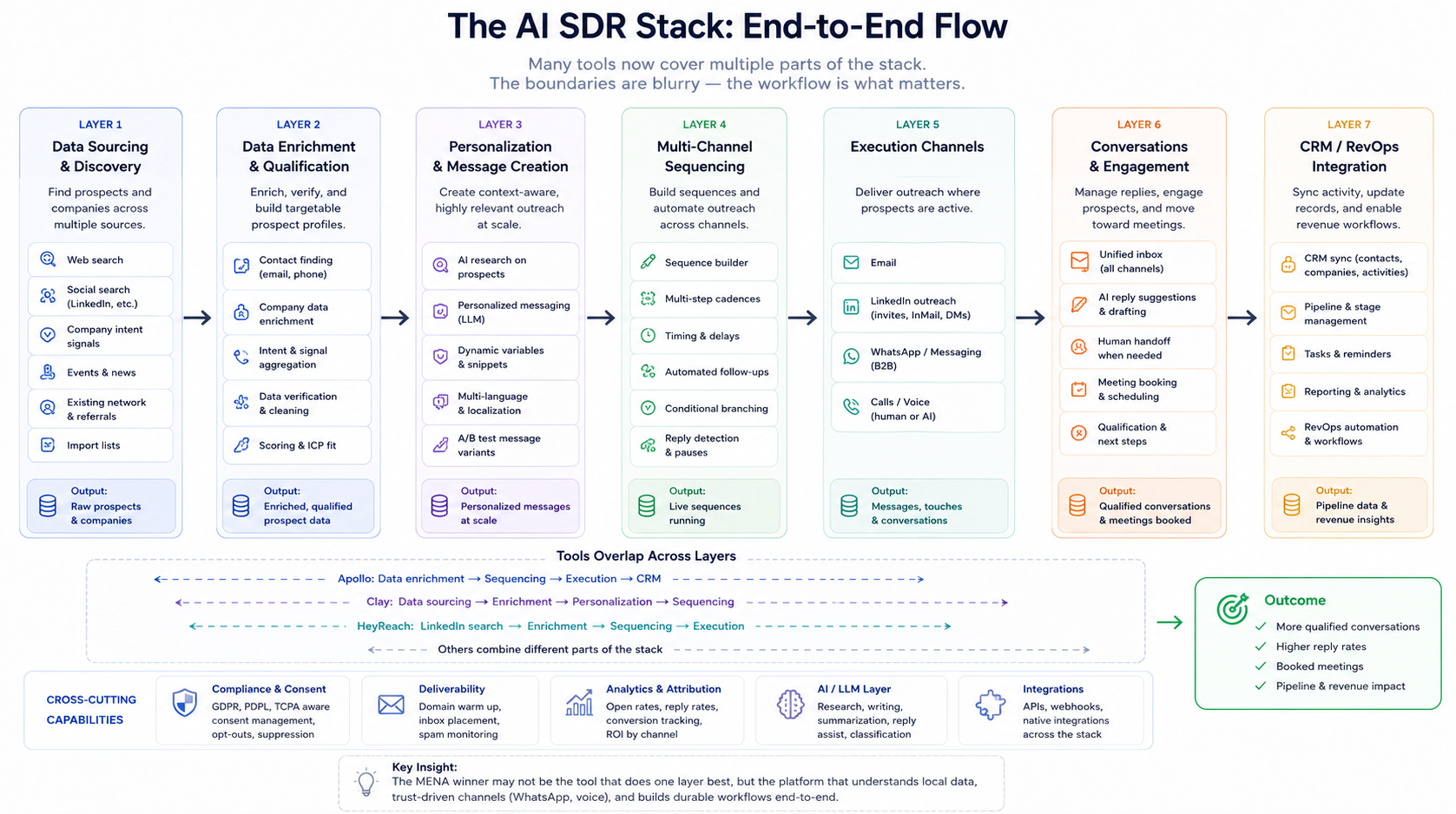

So the better way to map the AI SDR stack is by function. The functions are: source leads, enrich and qualify data, personalize the message, build sequences, choose the channel, engage in conversations, book meetings, sync the CRM, and learn from outcomes. The companies then bundle across these functions in different ways.

That distinction matters as an investor. A vendor may touch five parts of the workflow, but that does not mean it owns five moats. The underwriting question is not “which layer is this company in?” The better question is: where is the wedge? Where is the dependency? Where is the control point? And which part of the workflow would be painful for the customer to rip out?

My current view is simple: the US winner in this category may be an AI-native outbound platform optimized for scale. The MENA winner may need to be something different. It may need to own trust. And in this region, trust often does not start with a cold email. It starts with WhatsApp, a warm introduction, a voice note, or a real call.

The stack is really a workflow

The old way to map this category is as a vertical stack of companies. Raw data at the bottom. Contact databases above that. Enrichment tools above that. Personalization tools above that. Channels above that. AI SDRs above that. CRM at the end.

That map is useful, but incomplete. The market is blurring. Tools are expanding across the workflow because customers do not wake up wanting “a Layer 3 enrichment product.” They want qualified conversations, booked meetings, pipeline, and revenue.

So I now think of the stack as an end-to-end workflow.

First, you need to discover the right accounts and prospects.

Then you need to enrich and qualify them.

Then you need to understand context and personalize the message.

Then you need to build sequences and choose the right channels.

Then you need to manage replies, conversations, objections, and meeting booking.

Then everything has to sync back into the CRM or RevOps system.

And across the whole flow, you need compliance, consent, deliverability, domain and inbox reputation management, analytics, AI/LLM infrastructure, and integrations.

The more I look at the market, the more I think the important question is not whether a company covers one layer or many. Many will cover many. The important question is which function creates the control point.

Function 1: Data sourcing and discovery

Every outbound system starts with the same question: who should we contact?

This is where I think it is important to separate two very different types of companies.

The first group is the data wholesalers.

These are companies that collect, structure, license, and sell large volumes of people, company, job, and web data. Their customers are often other platforms, data teams, or companies building applications on top. They are closer to infrastructure than workflow software. Examples include companies like People Data Labs, Coresignal, Pipl, Bright Data, and other large-scale data providers.

The second group is the application layer built on top of data.

These are the tools sales teams actually use day to day: Apollo, ZoomInfo, RocketReach, Lusha, Cognism, Hunter, Amplemarket, and others. Some of them own or aggregate large databases. Some license data from wholesalers. Some combine multiple sources. Some add sequencing, calling, LinkedIn touches, enrichment, intent, and CRM syncing.

That distinction matters. A data wholesaler sells the raw material. An application-layer platform turns that raw material into a workflow. But both groups face the same hard problem: professional data decays quickly. People change jobs. Titles change. Companies restructure. Employees leave. Startups shut down. Teams expand. Phone numbers stop working. Emails bounce. A contact database is not a static asset. It is a living system that has to be constantly refreshed.

And in B2B, the most important refresh surface is usually LinkedIn. LinkedIn is where people update their job titles, employers, locations, promotions, and company affiliations. It is also where company pages, employee counts, hiring activity, and professional relationships become visible. So if you are trying to maintain a fresh professional database, LinkedIn becomes the gravitational center of the data-refresh problem.

That creates a strange tension. The most valuable source of professional truth is also a platform that does not want uncontrolled automated extraction on top of its network. This is why updating professional data is operationally hard. It is not just about collecting data once. It is about repeatedly checking whether a person is still at the company, whether their title changed, whether the company headcount shifted, whether a new VP joined, whether an old contact moved, and whether the org chart still makes sense.

Some of that can come from public web pages, company sites, filings, email verification, user-contributed data, and third-party partnerships. But a lot of the freshest professional identity data still points back to LinkedIn.

And the methods used to access that data sit on a spectrum. At the clean end, you have licensed datasets, public web data, customer-contributed data, user-permissioned workflows, and compliant enrichment partnerships. At the aggressive end, the industry has long had a shadow layer of scraping, automation, logged-in access, and account networks. LinkedIn has alleged in lawsuits that some scraping operations create large numbers of fake accounts to access and scrape profile and company data before LinkedIn detects and restricts them.

I would be careful not to assume every data provider uses the same methods. They do not. Some are more compliant than others. Some rely more on licensing and partnerships. Some rely more on crawling and scraping. Some are black boxes.

But as an investor, I would want to understand the data-refresh engine very deeply.

Where does the data actually come from?

How often is it refreshed?

How much is first-party, licensed, scraped, inferred, or user-contributed?

How dependent is the company on LinkedIn?

What happens if LinkedIn tightens enforcement?

Can the company verify MENA contacts without relying only on US/EU-weighted global datasets?

Can it update Arabic names, regional titles, holding-company structures, and family-business org charts accurately?

This is where MENA becomes interesting. When I search MENA contacts on global databases, I often find outdated titles, old companies, missing phone numbers, or incomplete records.

That is not necessarily because these products are bad. It is because their refresh economics are rational. If most of your paying customers are in the US and Europe, your refresh cycles will naturally prioritize those markets. Re-verifying a record in Riyadh may cost as much as re-verifying one in Austin, but the revenue pool behind Austin is much larger. So the record may have been accurate when first scraped. It just never received enough update passes.

That creates a potential opening for a MENA-native data layer. Not because the global incumbents cannot technically build better regional data, but because they may not be economically motivated to care enough.

The company I would be most interested in is not simply the one with the biggest database. It is the one with the best refresh loop. Because in this market, data quality is not about how many contacts you claim to have. It is about how often reality catches up to your database.

Function 2: Enrichment and qualification

Finding a name is not enough. You need to know whether the person is still in the role. Whether the email works. Whether the phone number is valid. Whether the company fits your ICP. Whether there is intent. Whether there is a relevant trigger. Whether this is the right time to reach out. That is where enrichment and qualification come in. This used to be a relatively simple function: append missing fields, verify emails, clean the list, maybe score the account. Now it is becoming more dynamic.

Clay is the obvious company to study here. It lets users combine multiple data sources, run waterfall logic, enrich records, validate data, and chain AI actions inside the workflow. That is powerful because no single data source is complete. One provider may have the email. Another may have the phone number. Another may have better company data. Another may have a more useful signal.

But again, Clay does not stop at enrichment. It now touches data sourcing, AI research, personalization, and downstream workflow automation. That is why I think of Clay less as “an enrichment company” and more as a flexible GTM orchestration layer.

Apollo also touches enrichment. HeyReach can touch enrichment through LinkedIn-based prospect data and campaign workflows. Many tools are moving toward the same center.

The underwriting question is: does the company simply enrich data, or does it become the place where GTM teams decide who deserves attention? That second position is much more interesting.

Function 3: Personalization and message creation

Personalization used to mean inserting a first name, company name, job title, and maybe one sentence about the prospect’s industry.

Now it means something else. Systems can read a prospect’s LinkedIn activity, company news, funding announcements, hiring patterns, tech stack, podcast appearances, public content, or recent events, then generate outreach that feels at least somewhat contextual.

But I am skeptical that “personalization” remains a standalone category for long. It feels more like a function that gets absorbed into the broader workflow. Clay can personalize. Apollo can personalize. Full-stack AI SDRs can personalize. Even channel tools can increasingly personalize inside the sequence.

So the real question is not whether the message is personalized. The real question is whether the system understands enough context to know what should be said, to whom, through which channel, and at what moment. That is a much harder problem than generating a clever first line.

For MENA, personalization is also more complex than English-language copy. Language, dialect, seniority, culture, tone, and relationship context all matter. A message that looks “personalized” in a US SaaS context may still feel wrong in Saudi, the UAE, Jordan, Egypt, or Kuwait.

That is one reason I think the MENA opportunity cannot be reduced to “take the US AI SDR playbook and translate it into Arabic.”

Function 4: Sequencing and follow-up

Sequencing is where outbound becomes a system. A sequence defines the order of touches, timing, delays, follow-ups, conditions, pauses, and replies. It can be email-first, LinkedIn-first, WhatsApp-first, call-first, or multi-channel.

This is another area where tools overlap heavily. Apollo does sequencing and follow-ups. Outreach and Salesloft built large businesses around sales engagement. Smartlead, Instantly, Lemlist, and others focus heavily on email sequencing, replies, and deliverability. Clay can trigger workflows and push actions downstream. HeyReach helps execute LinkedIn sequences across multiple sender accounts.

So again, the category does not map cleanly into one company per layer. The question is: who owns the cadence logic?

If a company becomes the place where a GTM team designs, tests, and optimizes its outbound motion, that is a strong position. But if sequencing is just a feature inside a broader tool, it may be easier to commoditize.

In the US, sequencing has been shaped heavily by email and LinkedIn. In MENA, I think the winning sequence may need to look different. It may start with LinkedIn, move to WhatsApp, then call, then follow up with a voice note, then sync to CRM. Or it may start with a warm relationship trigger before any outbound happens. That is a very different motion from “five emails and two LinkedIn touches.”

Function 5: Execution channels

This is where the MENA question becomes more interesting. In the US, the dominant outbound motion has been built around email and LinkedIn. You build lists, enrich contacts, write sequences, warm domains, rotate inboxes, manage deliverability, and optimize conversion.

That playbook works in some markets. But I do not think it transfers perfectly into MENA. Email exists here, of course. LinkedIn matters, especially for B2B. But in many relationship-driven markets, serious commercial trust still tends to move through more personal channels: WhatsApp, calls, introductions, and voice. That changes the shape of the opportunity.

Let’s also talk about tools.

Email tooling is already crowded, but email also has its own hidden infrastructure layer: deliverability. Sending outbound at scale is not just about writing good emails or building the right sequence. It is also about making sure those emails actually reach the inbox.

That means warming up domains and inboxes, configuring SPF, DKIM, and DMARC, monitoring bounce rates, managing sender reputation, rotating inboxes, controlling send volume, checking spam placement, avoiding trigger words, validating email addresses before sending, and removing bad contacts quickly.

This is why tools like Smartlead, Instantly, Lemlist, Mailreach, Warmy, and others exist around the email execution layer. Some help teams warm up inboxes. Some manage multiple sending accounts. Some monitor deliverability. Some help rotate volume across inboxes and domains. Some combine warm-up, sequencing, and reply management in one workflow.

This part of the stack is easy to underestimate because it feels operational rather than strategic. But in practice, deliverability can become the difference between a working outbound machine and a spreadsheet of messages nobody sees.

It also changes the economics of email outbound. Email looks cheap at the message level, but serious outbound requires infrastructure: domains, inboxes, warm-up time, monitoring, verification, sequencing rules, and constant maintenance.

As an investor, I would treat email deliverability as a core part of the execution layer, not a side feature. If a company claims to drive outbound pipeline through email, I would want to understand how it protects sender reputation, manages bounce risk, handles spam placement, and adapts when Gmail, Outlook, or other providers tighten enforcement.

LinkedIn automation is useful, but it carries platform risk because LinkedIn does not want uncontrolled automation on top of its network. HeyReach is a good example of the LinkedIn execution layer, but also a good example of why these categories blur. I would not classify it as a contact database, and I would not classify it as a full-stack AI SDR. Its core wedge is execution: helping agencies and sales teams run LinkedIn outreach across multiple sender accounts, with sender rotation, unified inboxes, workspaces, API/webhooks, and integrations into the rest of the outbound stack.

But because LinkedIn is also a prospect discovery surface, HeyReach can sit closer to the start of the workflow than a simple “sending tool.” A team may use LinkedIn search to identify prospects, then use HeyReach to operationalize outreach across multiple accounts.

That makes HeyReach useful infrastructure for LinkedIn-led outbound, especially for agencies that need volume and operational control across many accounts. But it also shows the channel-risk problem clearly. The product scales by distributing activity across LinkedIn accounts while staying within per-account limits. That can work, but the underlying channel still belongs to LinkedIn.

WhatsApp is culturally powerful in MENA, but still underbuilt for B2B outbound. And calling remains expensive because every serious call requires either a human or a highly compliant, high-quality AI voice layer.

As an investor, I would not underwrite this as true channel ownership. I would underwrite it as a strong workflow layer sitting on top of a rented platform. This is where I think a regional product could look very different from a US product. The winning US company may optimize for scale. The winning MENA company may need to optimize for trust.

The platform-risk problem

LinkedIn is a good example of why channel ownership matters.

Many outbound tools sit on top of platforms they do not control. They automate user sessions, distribute activity across accounts, and try to stay within limits. That can work, but it introduces platform risk. If the underlying platform decides to enforce more aggressively, the tool’s value proposition can change overnight.

As an investor, that matters. I do not want to underwrite a company as if it owns distribution when, in reality, it is renting access from a platform that is actively trying to limit automation.

That does not mean LinkedIn automation tools are bad businesses. Some can be very useful, especially when they solve painful workflow problems for agencies and GTM teams. But the risk profile is different from a company that owns its own data layer, its own consented communication channel, or its own system of record.

Email has a different version of the same problem.

Email is more open than LinkedIn, but it is not permissionless in practice. Gmail, Outlook, and other providers constantly adjust spam filters, authentication rules, sending limits, and reputation signals. So even when you technically own the domain and inbox, you still operate inside an ecosystem controlled by large email providers. That makes deliverability a moving target.

WhatsApp has a similar tension.

The official WhatsApp Business API is gated through business partners, structured, permissioned, and template-driven. It is better suited for support, CRM workflows, and approved business messaging. Unofficial layers can move faster by connecting personal accounts, but they come with account risk and compliance risk.

So the question is not simply: can you automate WhatsApp? The better question is: can you build a compliant, durable, B2B-native WhatsApp workflow that fits how business actually gets done in the region? As far as I can tell, that is still not fully solved.

Function 6: Conversations and engagement

This may be the most underrated part of the stack. Outbound teams often obsess over the send: the list, the copy, the sequence, the channel. But the real value starts after someone responds. Can the system classify the reply? Can it understand intent? Can it handle objections? Can it route to a human? Can it book the meeting? Can it re-engage no-shows? Can it keep context across channels? Can it tell the difference between a polite “not now” and a real future opportunity?

This is where I think narrower products may sometimes outperform full-stack products. A company that only handles post-reply workflows may look less ambitious than an “AI SDR” that promises to replace the whole role. But if it owns the highest-intent part of the funnel, it may have better retention and clearer ROI.

This is also where the trust layer becomes visible. In MENA, the conversation may not happen in the same place as the first touch. A prospect may ignore the email, accept the LinkedIn request, reply on WhatsApp, ask for a call, then want a human introduction before moving forward.

A good MENA-native product would need to understand that journey. It cannot treat every channel as just another notification surface. The channels carry different levels of intimacy and trust.

Function 7: CRM and RevOps integration

The workflow does not end when a meeting is booked. The activity has to land somewhere. Contacts, companies, touches, replies, meetings, notes, tasks, and pipeline data all need to sync into the CRM or RevOps system. Salesforce, HubSpot, Microsoft Dynamics, Pipedrive, Attio, and newer AI-native systems all matter here.

But for a MENA-focused startup, I would be cautious about trying to build a new system of record too early. The better path may be to stay CRM-agnostic and integrate deeply with the systems customers already use. That is more capital-efficient and easier to sell. The CRM layer is powerful because it becomes the institutional memory of the revenue organization. But it is also a difficult place to compete directly unless you have a very clear wedge. For most AI SDR companies, I would rather see deep integrations than a premature attempt to replace the CRM.

Full-stack AI SDRs and the promise problem

Now we can talk about the flashiest part of the category: full-stack AI SDRs.

Companies like AiSDR, 11x, Artisan, Regie, Sybill, and others are trying to own much more of the workflow from prospecting to booked meeting. The promise is attractive: an AI worker that sources leads, enriches them, writes messages, follows up, handles replies, books meetings, and updates systems.

The problem is that the promise can easily get ahead of the product. That is not specific to one company. It is a category risk. When a product claims it can replace an SDR team, expectations become very high. If the product behaves like a workflow assistant instead of a full replacement, churn can become painful.

One case study I would study carefully here is 11x. The company became one of the most visible examples of the “AI SDR” promise: a digital worker that could take on a large part of outbound prospecting. But the controversy around the company also shows why this category needs careful underwriting. Reported revenue, logo quality, customer retention, and the difference between trial usage and durable ARR all matter enormously when a product is selling replacement-level ambition.

I am not bringing this up to make the point about one company. I think the broader lesson is more important. In AI SDR, the bigger the promise, the bigger the gap when reality undershoots. A tool that says “we help your SDR team do more” is judged differently from a tool that implies “we replace your SDR team.” The second promise may sell faster, but it also creates a much higher bar for retention, expansion, and customer trust.

So whenever I look at a full-stack AI SDR company, I would want to dig hard into the quality of revenue:

How much of ARR is past the trial period?

What percentage of customers are active after three and six months?

Are the meetings converting into opportunities?

Are logos paying customers or pilots?

Is churn hidden by new sales velocity?

And are customers buying the product as workflow leverage, or as a headcount replacement fantasy?

This is one of the biggest underwriting questions for me in this space.

I would want to understand retention very deeply. Not just ARR. Not just logos. Not just “meetings booked.” I would want to know:

Are customers expanding after three months?

Are they still active after six months?

Are booked meetings converting into real opportunities?

Are customers using it as a replacement for people, or as leverage for existing teams?

Does the product create trust, or just more outbound noise?

The more ambitious the product promise, the more careful I would be with the revenue quality.

The legal wall around AI calling

Voice is one of the most interesting parts of the stack, but also one of the most legally sensitive.

In the US, AI-generated voice calls are subject to serious restrictions under the TCPA framework. The FCC has made clear that AI-generated voices fall under rules governing artificial or prerecorded voices. In practice, that means AI voice companies need to be very thoughtful about consent, especially when calling mobile numbers.

That matters even outside the US because it shows where the market is likely going: AI voice will not be allowed to behave like an unlimited cold-call machine forever. Serious companies in this space will need consent capture, compliance workflows, audit trails, opt-out logic, and careful call design built into the product from day one.

That is why I do not think the opportunity is simply “AI that cold-calls everyone.” The better opportunity may be signal-triggered, consent-aware, relationship-based calling.

For MENA, this becomes even more interesting because voice can be a trust channel, not just a sales channel. A good call in the right Arabic dialect can do things that email cannot.

Which brings me to the regional opportunity.

Why MENA may need a different winner

The US AI SDR market is shaped by the economics of scaled SaaS outbound.

High-volume email.

LinkedIn sequencing.

Automated personalization.

Large TAMs.

Standardized buying motions.

A lot of the innovation is about making the machine faster, cheaper, and more automated.

But MENA is not just a smaller version of the US market. The region has different trust patterns, different communication norms, different language complexity, and different sales culture. In many cases, business still moves through relationships. A WhatsApp message may outperform an email. A warm call may matter more than a beautifully personalized sequence. Dialect can matter more than generic “Arabic support.”

That means a MENA-native AI SDR company may need four things that are not necessarily central to the US playbook.

First, better regional data.

Not just more contacts, but fresher contacts. Better phone number coverage. Better company mapping. Better Arabic and English naming resolution. Better understanding of family businesses, holding companies, semi-government entities, and regional org structures.

Second, WhatsApp-native workflows.

Not a hacked consumer workflow. Not only support templates. A real B2B system for compliant outreach, follow-up, reminders, routing, and relationship management.

Third, dialect-fluent voice.

Not “Arabic” as one language checkbox. Gulf Arabic, Saudi nuance, Emirati nuance, Levantine nuance, Egyptian nuance. The difference matters if voice is supposed to build trust rather than just transmit information.

Fourth, CRM-agnostic integration.

I don’t think it’s wise for a MENA AI SDR startup to fight Salesforce, HubSpot, Microsoft, or whatever CRM the customer already uses. The more capital-efficient path is probably to integrate deeply into existing systems, or new internally vibe-coded systems, rather than build a new system of record from scratch.

Calling may be the moat, not the cost center

In most outbound models, calling is treated as expensive. Email is cheap. LinkedIn is semi-scalable. Calling is labor-intensive. But in MENA, that cost may be exactly what creates the moat. Anyone can send more emails. Anyone can spin up more sequences. Anyone can write another AI-generated first line. But not everyone can create a high-quality, compliant, dialect-aware calling layer that actually improves trust and moves a buyer forward.

That is harder to build. It is also harder to rip out once it works. If a company becomes the layer that manages your trusted outbound conversations across WhatsApp, phone, CRM, and follow-up, then it is no longer just another sales automation tool. It becomes part of the commercial operating system.

That is the kind of product I would be much more interested in.

The bear case: cold outbound may be getting worse

It is important to take the bear case seriously. Cold outbound is under pressure. Buyers are overwhelmed. Inboxes are saturated. AI-generated messages are making the noise problem worse. The more everyone automates, the less differentiated automation becomes.

That does not mean outbound dies. But it probably means the market shifts from blind volume to better timing. The future may be less about “send 100,000 messages” and more about “know exactly when to reach out, through the right channel, with the right context, and with enough trust to earn a response.”

That is why I like the idea of relationship-intent more than pure cold prospecting. A known contact changing jobs. A portfolio company expanding into Saudi. A founder hiring a head of sales. A company raising a new round. A buyer attending an event. A government entity launching a relevant initiative. These are not random cold moments. They are trigger moments.

A MENA-native platform should probably be built around those moments.

Where I would put capital

If I were underwriting this category, I would not start by asking, “Who has the best AI SDR?”

I would ask a different set of questions.

Does the company own a trust channel, or only a volume channel?

Does it have a real regional data advantage, or is it reselling the same global databases?

Does it have a refresh loop that can keep regional data current?

How dependent is it on LinkedIn, and what happens if that access gets restricted?

Does it support WhatsApp in a durable and compliant way?

Does it have a serious calling layer, or is voice just a demo feature?

Can it understand dialects well enough to matter commercially?

Does it integrate with the customer’s CRM instead of trying to replace it too early?

Are retention and expansion strong after the initial AI excitement fades?

Can the team explain why they are not just building a faster spam machine?

The companies I would be most interested in are not necessarily the ones with the loudest “AI worker” branding. I would be more interested in the ones that understand the full revenue workflow, respect the regional trust layer, and know where automation should stop.

The white space

As far as I can tell, nobody has fully built the MENA-native version of this, yet.

There are companies attacking parts of the workflow: data, enrichment, LinkedIn automation, email sequencing, deliverability, reply handling, voice infrastructure, Arabic voice, CRM automation. But I have not yet seen the company that combines the full workflow:

Regional data.

A durable refresh loop.

Email deliverability.

WhatsApp-native sequencing.

Compliant calling.

Arabic dialect quality.

Post-reply handling.

CRM-grade follow-up.

All built for MENA from day one.

That is the white space I would keep watching. The endgame is probably not “AI replaces the SDR.” That framing is too simple. The more interesting endgame is that AI collapses the mechanical parts of outbound: list-building, enrichment, research, drafting, routing, follow-up, CRM updates. But the trust-dependent parts remain scarce.

In the US, maybe the winning product is the best autonomous outbound machine.

In MENA, I think the winner may look different. It may be the company that understands that selling here is not just about reaching the buyer. It is about earning the conversation.